Measuring Return

Cap Rates and Cash on Cash

You don’t need a college degree to be an investor but you need to set goals and know how to assess how a property should perform against those goals. In this lesson we will cover your return on investment calculations and we promise not to overwhelm or bore you.

So please read on.

The purpose of measuring the "return on investment" (ROI) metric is to quantify the rates of return on your money invested in a property and compare it to 1) your goals, 2) another property and 3) to an alternative investment vehicle like the stock market. But note there are different levels of risk, asset appreciation and tax implications for all types of investments.

Measuring return provides a snapshot of profitability and cash flow and the first metric we need to understand is the capitalization rate

Capitalization Rate

The capitalization rate (cap rate) is the ratio between the net operating income produced by a property and the original price you paid, expressed as a percentage. Does that sound a little complicated? Don’t worry let’s dig in and I’ll keep it real world and simple.

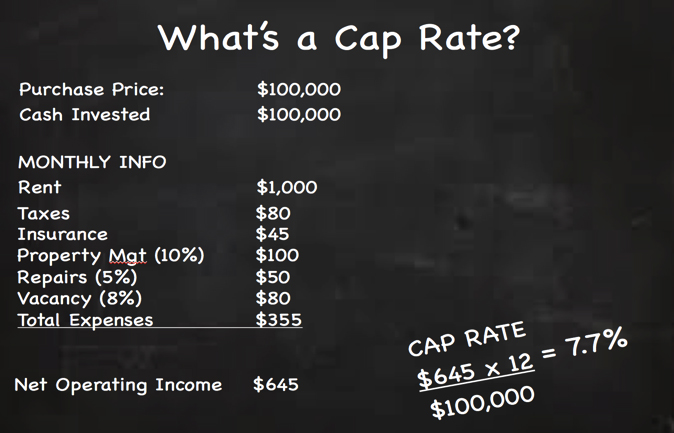

Assume you buy a $100,000 property renting for $1,000 per month

Let’s assume you are looking at an investment property with a purchase price of $100,000. You’ll have some purchasing costs like an inspection report and title insurance but lets keep it simple and assume a total cash investment of $100,000. This property is rented for $1,000 per month so we know your projected rental income.

Estimating your expenses

Let’s look at this property’s expenses broken down into a monthly view. The annual property tax is $1,000 (verified online with local county records) and is budgeted at $80 per month, even though the county bills it twice a year. Your landlord annual insurance premium is $550 for dwelling coverage and personal liability, and is a $45 per month expense. Your property manager charges 10% of gross rent received, so that’s $100 per month. Now comes the tricky part--your estimate for repairs and vacancy rates (time your rental is not leased).

Vacancy and maintenance estimates are a little tricky

Estimating your repair and maintenance costs depends upon the property type (condos are lower for example), condition of the property, location, tenants, etc. It can be calculated based on a percent of the value of the property or as a percent of your rental income. In the example below we assume $600 per year and 5 percent of rental income because the property has been recently renovated.

Finally we want to add an expense to account for the period in between leases where this property will be vacant. A “vacancy rate”’ is usually expressed as a percent of rent and recorded as a dollar amount in your budget. The national average is 8 percent but varies in each metropolitan area and neighborhood, so in this example we will assume 8 percent. We also provide vacancy rate analysis in our market reports like the data below so we can see trends for city, state and US averages.

Now, look at your chalkboard summary below for a monthly snapshot. Please note that this is an average and our actual income and

expenses will be “lumpy” because vacancies and repair expenses don’t smooth out evenly throughout the year. However, it should look something like this.

Measuring Your Cap Rate

Calculating Your Net Operating Income

So now that we have your projected income and expenses we can calculate your Net Operating Income (NOI). Your income is $1,000 per month and expenses are $355 so your Net Operating Income is $645 per month and $7,740 per year. Cap rates measure the annual net operating income produced by a property as a percentage of the original price paid. In this case it’s $7,740 divided by $100,000,

which is a 7.7% return.

Cash on Cash

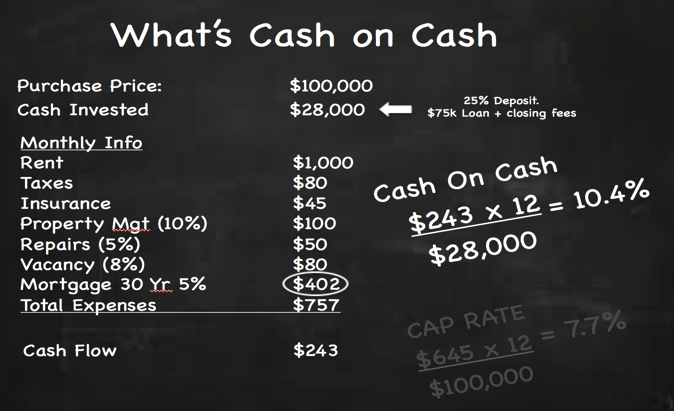

Once you have a cap rate you can move on to look at the opportunity to get financing and borrow some of the purchasing funds and look at cash-on-cash return. The cash-on-cash return is the ratio of annual before-tax cash flow to the total amount of cash invested, expressed as a percentage. As a rule of thumb, if your interest rate is lower than the cap rate then your cash on cash will be a better return. Let’s dig in.

Assume you decide to borrow 75 percent of the purchase price and place 25 percent down as deposit. With closing costs of $3,000 your out-of-pocket cash is $28,000 with a mortgage of $75,000. Your new mortgage payment is $402 per month and with that additional expense you will clear $243 of cash flow per month or $2,916 per year. Now to measure your cash-on-cash return, simply divide your annual cash flow of $2,916 by the total cash invested of $28,000 and voila, your cash on cash return is 10.4 percent. By borrowing at a lower rate than your cap rate you use less funds to buy the property and your return significantly increases. This is leverage. In addition, the interest paid on your mortgage is a deductible tax expense, which we will explain later.

Leveraging a Mortgage and Calculating Your Cash-on-Cash Return

SUMMARY

- There are two key measurements for return: Capitalization Rate and Cash on Cash

- The Capitalization Rate is the ratio between the net operating income and the purchase price expressed as a percentage

- The Cash-on-Cash Return is the ratio of annual before-tax cash flow to the total amount of cash invested

- Actual income and expenses don’t smooth out evenly throughout the year and are “lumpy” in nature

Clear demonstration of the computation. So far, this is my favorite section.

Love this section! I have thumbed through multiple books about real estate investing and have never seen these terms explained so simply and easy to understand. Thank you!!

Brilliant! Once you have the numbers down the rest is about diligence on the market and the specific property!

concise, simple calcs to show how to get at a good starting number to figure out if you’re looking at a keeper investment. Helpful homework, I didn’t finish! Just signed refi docs yesterday! Ha

Hey thanks for feedback and love that you like the homework. we feel it keeps you accountable to hitting your goals. Congratulations on the refi.